One Junior Partner in Atlantic Yards is Suing Another, for $888M. That's Alarming.

Affiliates of the U.S. Immigration Fund and Fortress Investment Group are fighting over a separate project. Shouldn't we know more about their stake, and clout, in Atlantic Yards?

What does it mean that the two key junior partners in Atlantic Yards/Pacific Park, affiliates of the U.S. Immigration Fund (USIF) and Fortress Investment Group, are adversaries in a lawsuit charging that a mere $888 million is owed regarding a separate—but semi-related—real-estate deal?

Nothing good, especially since the USIF, which is itself ethically tarnished, charges “financial behemoth” Fortress with acting “in bad faith.” (Fortress is majority owned by Abu Dhabi-based, state-owned sovereign wealth fund, Mubadala, though its management, which owns 32%, controls its board.)

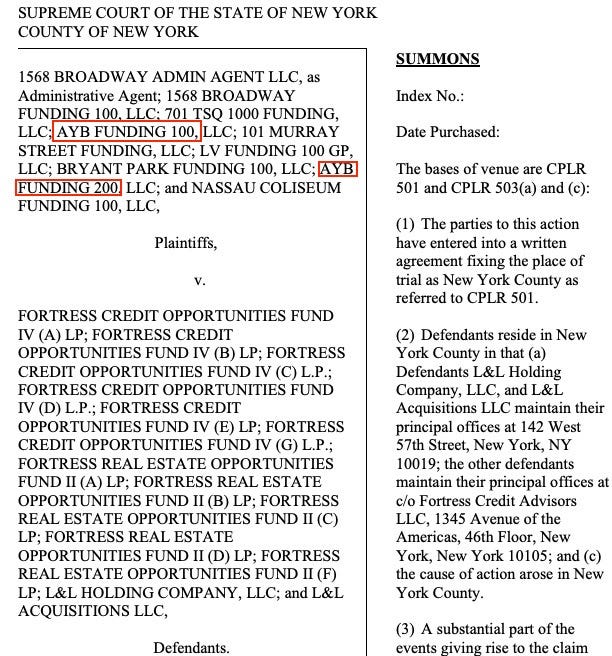

Here’s the case, 1568 BROADWAY ADMIN AGENT LLC et al v. FORTRESS CREDIT OPPORTUNITIES FUND IV (A) LP et al, involving a Times Square hotel, retail, and theater complex, TSX Broadway. Kathryn Brenzel broke the news Feb. 19 in The Real Deal, Lawsuit claims Fortress, L&L owe USIF $890M after TSX Broadway transfer.

The lawsuit contends that at least one counter-party is not trustworthy, and reminds us, not surprisingly, that maximizing their financial returns--not any purported public benefit--is the parties’ priority.

That’s concerning for Atlantic Yards watchers, and should be concerning for Empire State Development (ESD), the state authority overseeing/shepherding the project. ESD is currently negotiating a Memorandum of Understanding regarding public support—subsidies, tax breaks, and additional free bulk—for the project.

Murky stakes

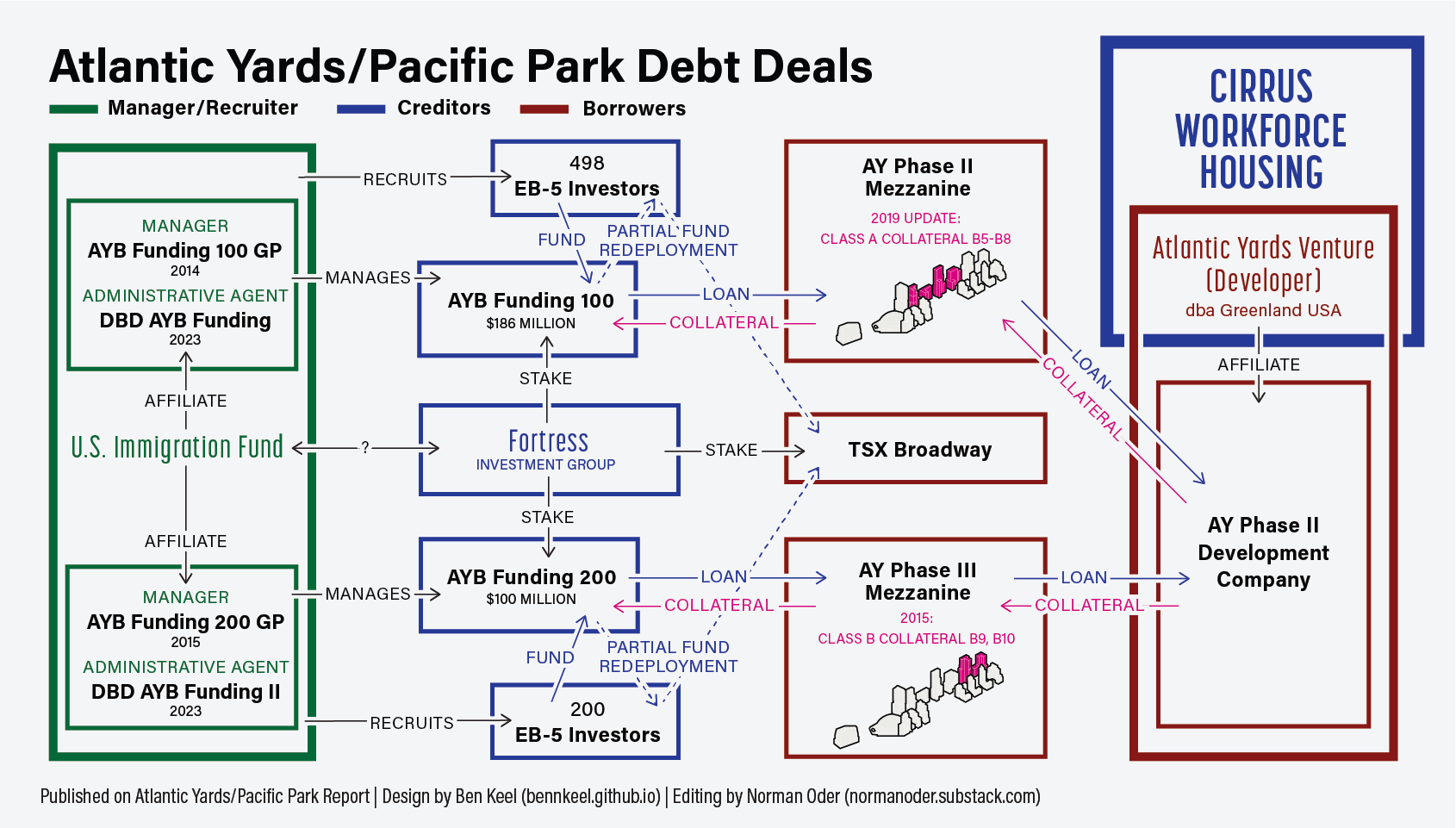

Worse, we still don’t know anything about those parties’ financial stakes, and clout, in the new Atlantic Yards configuration, which is led by funder Cirrus Workforce Housing, in partnership with developer LCOR, but also involves USIF, Fortress, and original developer Greenland USA.

Cirrus has said that Greenland is at the back of the line for any potential financial returns. It hasn’t spoken similarly about the USIF and Fortress.

Remember, Cirrus acquired $200 million of Greenland USA’s debt, at a discount, to leverage the project, proposing an additional 1.6 million of bulk, and yet unspecified subsidies and tax breaks, to make the project feasible.

(I’ve argued that we should better understand their cost basis before granting such concessions.)

Cirrus acquired outstanding debt on Atlantic Yards, excepting the even larger amount of debt Greenland borrowed from immigrant investors from China under the EB-5 investor visa program.

That debt, some $286 million (plus likely a good chunk of interest), is controlled by affiliates of the USIF, the “regional center” that organized the EB-5 investments, as well as Fortress, which acquired a stake.

The immigrant investors, who put the money up, have little control, thanks to disadvantageous contracts that leave the Manager, led by the USIF’s Nicholas Mastroianni II, with his “checkered past,” with key decision-making power.

A “Prohibited Person”?

Back up for a moment. It’s still unclear whether/how ESD concluded that the USIF’s Mastroianni was not a “Prohibited Person” with a felony record, which would bar him from doing business with New York State.

Mastroianni in his younger days was arrested on felony drug charges and pleaded no contest, but it’s unclear whether the plea was to a felony—or whether the record was later expunged.

How could Mastroianni be part of a “permitted developer,” local resident Robert Puca asked at a meeting in November 2024 of the advisory Atlantic Yards Community Development Corporation (AY CDC), when the USIF was expected to be part of a joint venture not with Cirrus but with Related Companies.

“We’re still looking at it,” said ESD lawyer Matthew Acocella. “But based on the information we’ve gotten and based on the structure of the [joint venture], we don’t see any any bar to proceeding with this joint venture as the permitted developer with Related and USIF.”

No further information has surfaced about that joint venture, or the new one led by Cirrus, regarding the USIF’s role.

Ownership, and leverage

If Cirrus paid 50 cents on the dollar for Greenland’s debt, it spent $100 million. Yes, it has significant other expenses (project debts, lawyers, architects/planners, lobbyists, environmental review, payments to the MTA for development rights) to advance the deal.

Whether Cirrus paid $100 million, $120 million, or even $80 million, that figure is dwarfed by the $286+ million in EB-5 debt, held by AYB Funding 100 and AYB Funding 200, which immigrant investors funded, as well as Fortress. Those latter creditors must have some significant stake.

Cirrus principal Joseph McDonnell called the deal a “no-brainer.” I suggested that it fit their goal of “investments that offer asymmetric risk-return profiles and significant downside protection.”

The EB-5 investors purportedly had collateral in Greenland affiliates with the rights to build towers over the Metropolitan Transportation Authority’s Vanderbilt Yard. That was somehow trumped by Cirrus’s stake.

Still, it seems likely that the USIF affiliates and Fortress have a reasonably robust stake in the future project, including financial returns, even if they don’t manage the project. It may include some role in raising funds, deciding to start a building, or entering into new joint ventures or property sales.

Some checkered history

The history of joint ventures with Atlantic Yards is somewhat fraught.

When Greenland USA in 2014 bought a majority share of the project going forward, the agreement with original developer Forest City Ratner required each partner’s assent on major decisions, and also provided for dilution of member’s interest if it failed to meet certain obligations, as ESD explained in a memo.

So the proposed 70/30 equity split going forward, the memo stated, “may be subject to change.” That it was. Forest City later exited the project almost completely, after apparent tension between the two and years of stalling.

Is the proposed equity split between Cirrus/LCOR and USIF/Fortress 70/30? What’s the effect of USIF and Fortress suing each other? What’s the exit process?

How Fortress entered

During the pandemic, with Atlantic Yards stalled, the USIF encouraged the EB-5 investors in AYB Funding 100 to move up to $150 million to TSX Broadway and those in AYB Funding 200 to move up to $50 million.

(Updated and clarified) Before that, in 2019, the sale of one development lease required those EB-5 investors to redeploy a fraction of their funds to another project, as shown in the screenshot below.

The USIF offered both a carrot and a stick. The carrot was a purportedly better investment, based on economic conditions and risks. The stick was a warning that Fortress would be in control of those Atlantic Yards EB-5 funds.

If TSX Broadway was, as USIF then contended, a more solid project than Atlantic Yards, why would Fortress move extra cash—or, at least seek a stake—in the Brooklyn project? Either TSX was unsteady—indeed, it would crash—or Fortress saw Atlantic Yards as advantageous. Maybe both.

Note that investors were told that the latest their capital would be returned would be 45 months, with two optional extensions of 12 months—or nearly six years. That seems very much in doubt.

What now?

This lawsuit should be a yellow light, if not a red one, for Empire State Development.

Given the fraught history of Atlantic Yards, the public deserves to know, before government agencies make any commitments, more about the stakes, and decision-making power, in Brooklyn Ascending LandCo, the Cirrus-led LLC that apparently controls the project.

What percentages do the USIF affiliates and Fortress have?

What decision-making power do they have?

How much room is there for such litigious, and financially-driven parties, to bend Atlantic Yards to their own interests?

How much should we trust the USIF (which claims Fortress is in the wrong), given its checkered history?

These seem natural questions for the AY CDC, which is supposed to meet quarterly and advise ESD. Some AY CDC Directors occasionally float tough questions. The body last met on Dec. 2, so an early March meeting may be in order.

(Maybe they also kind ask about why so little of the AY CDC’s budget has been spent.)

More on the lawsuit

The lawsuit alleges that, from Dec. 7, 2018, until Dec. 15, 2021, the plaintiffs, an administrative agent as well asinvestment funds formed by the USIF to deploy EB-5 investors’ money, advanced about $520 million to “mezzanine borrowers” —subordinate to other loans—as part of the financing for the $2.5 billion TSX Broadway.

Those borrowers, the lawsuit alleges, now owe nearly $888 million in principal and interest. The defendants include affiliates of Fortress as well as developer L&L Holding Co.

The liability, the plaintiffs claim, was triggered in 2024 when the borrowers made an improper deal for Goldman Sachs to take over the project.

The lawsuit alleges that the defendants and their affiliates “lulled and misled Administrative Agent to believe that the entire Project financing, including the Mezzanine Loan, was being restructured.”

Had the Administrative Agent enforced its contractual remedies, the borrowers/defendants would have had to go to court, involving “foreclosure proceedings that would trigger massive transfer tax liabilities in the tens of millions of dollars.”

Harsh words

“Neither financial behemoth involved here, Fortress or Goldman Sachs, wanted to pay the transfer taxes or concern themselves with the hundreds of millions of dollars invested by the foreign investors and Plaintiffs, so they acted in bad faith,” the lawsuit alleges. It even charges that the defendants misled the plaintiffs by providing “redacted documents hiding critical provisions.”

The plaintiffs even claim a whistleblower: “A former senior officer of Fortress admitted that the transaction was designed and implemented in order to deprive Plaintiffs of their bargained-for rights.” So only did the plaintiffs lose money, “the taxpayers and citizens of New York were deprived of tens of millions of dollars” in transfer taxes.

(When it serves their interest, such parties can sound civic-minded.)

The lawsuit, it should be noted, is one side’s allegations, and has not yet triggered a response in court. A Fortress spokesperson told The Real Deal the firm considers the lawsuit “without merit.” L&L and Goldman wouldn’t comment.

Their defense might challenge the plaintiffs’ actions or credibility. If so, that would mean allegations, perhaps via sworn documents, that neither the USIF nor Fortress is particularly trustworthy.

If so, why is New York State not just doing business with them, but negotiating gifts of public resources?

Given delays have costs what is the likelihood of any clarification prior to scheduled ESD decisions that keep the project moving forward? Outside of the AY CDC is there room or place for a community response, or demand for clarity, to this uncertainty?